Futures Market: On the evening of last Wednesday, LME copper opened at $9,230/mt, initially touching a high of $9,243/mt before fluctuating downward. It hit a low of $9,103/mt near the close and eventually settled at $9,446/mt, up 0.22%. Trading volume reached 700 lots, and open interest stood at 287,000 lots. SHFE copper was closed on the evening of last Wednesday.

[SMM Copper Morning Meeting Summary] News: (1) On Monday, May 5, data released by ISM showed that activity among US service providers accelerated in April after a sharp decline in March, with raw material prices rising due to tariff increases. The US ISM Services PMI for April was 51.6, exceeding expectations of 50.3 and the previous reading of 50.8, which had unexpectedly fallen to a nine-month low. 50 is the demarcation line between expansion and contraction. The latest data outperformed predictions from the vast majority of economists surveyed by the media.

(2) From the beginning of 2025 to 0:00 on May 5, the trade-in policy was well-received, with over 3 million applications for auto trade-in subsidies. Consumers purchased 55.16 million units of 12 major categories of home appliances through trade-in programs and 41.67 million digital products such as mobile phones. In the first four days of the holiday, auto trade-in subsidy applications exceeded 60,000, driving new car sales worth 8.8 billion yuan. Consumers bought 3.56 million units of 12 major categories of home appliances, generating 11.9 billion yuan in sales, and purchased 2.42 million digital products such as mobile phones, driving 6.4 billion yuan in sales.

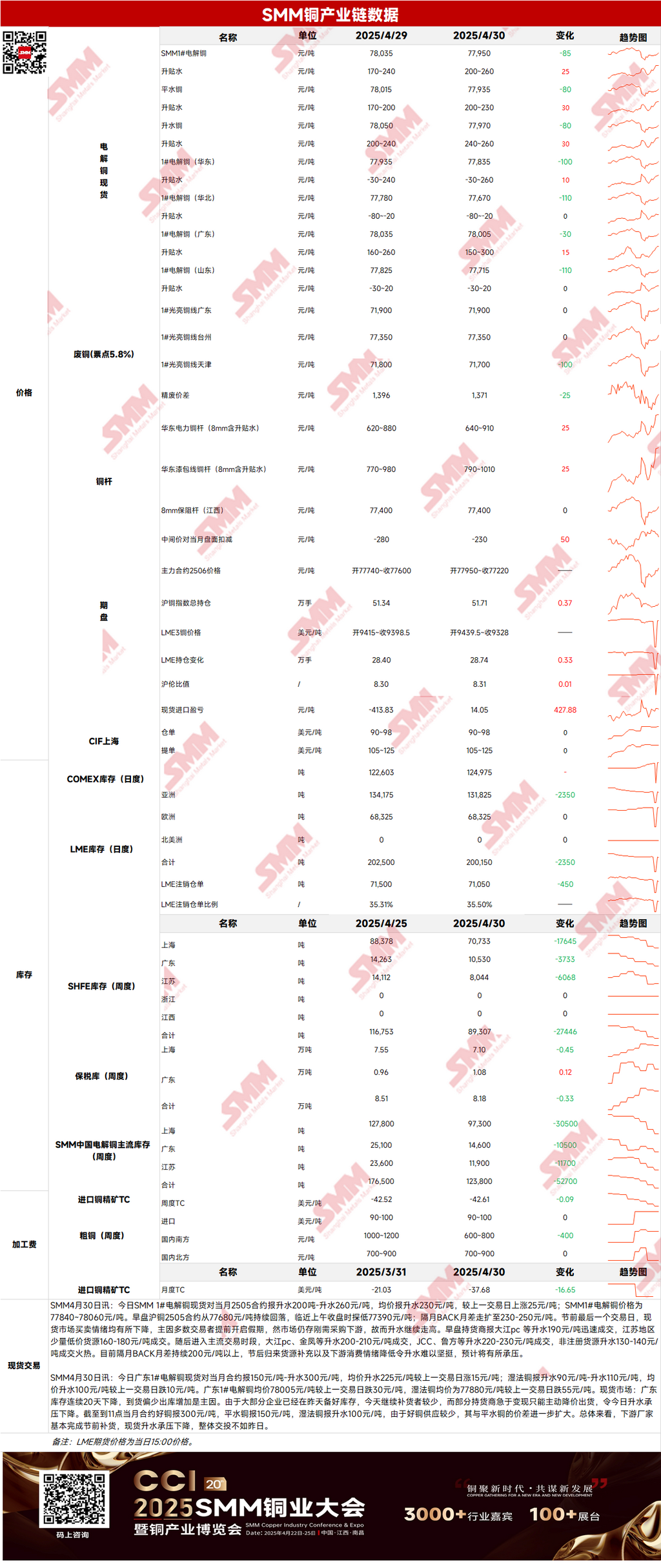

Spot Market: (1) Shanghai: On April 30, SMM #1 copper cathode spot prices were quoted at a premium of 200-260 yuan/mt against the front-month 2505 contract, with an average premium of 230 yuan/mt, up 25 yuan/mt WoW. On the last trading day before the holiday, buying and selling sentiment in the spot market declined, mainly due to most traders starting their holidays early. However, downstream demand for just-in-time procurement remained, causing premiums to continue rising.

(2) Guangdong: On April 30, Guangdong #1 copper cathode spot prices were quoted at a premium of 150-300 yuan/mt against the front-month contract, with an average premium of 225 yuan/mt, up 15 yuan/mt WoW. Overall, downstream manufacturers had largely completed their pre-holiday restocking, leading to a decline in spot premiums under pressure. Trading activity was weaker compared to April 29.

(3) Imported Copper: On April 30, warrant prices were $90-98/mt, with a QP of May, and the average price remained unchanged WoW. B/L prices were $105-125/mt, with a QP of May, and the average price remained unchanged WoW. EQ copper (CIF B/L) was priced at $65-75/mt, with a QP of May, and the average price remained unchanged WoW. Quotations referenced cargo arrivals in early May. Spot trading was relatively sluggish before the Labour Day holiday, with some traders inactive due to month-end financial settlements. According to market news, Glencore's Altonorte smelter is expected to extend its maintenance plan until May, with the specific end date of the maintenance yet to be determined. The market is concerned that this maintenance may affect electrolytic copper production in South America, exacerbating the current tight supply of copper elements.

(4) Secondary Copper: On April 30, secondary copper raw material prices remained unchanged WoW. Guangdong bare bright copper prices were 71,800-72,000 yuan/mt, unchanged from the previous trading day. The price difference between copper cathode and copper scrap was 1,371 yuan/mt, up 23 yuan/mt WoW. The price difference between copper cathode rod and secondary copper rod was 1,005 yuan/mt. According to SMM surveys, imported secondary copper raw material quotations remained high, with domestic traders unable to accept overseas offer prices. High prices, combined with weak demand during the off-season, are expected to lead to a larger-than-expected decline in secondary copper raw material port arrivals in May and June.

(5) Inventory: On April 30, LME copper cathode inventory decreased by 2,350 mt to 200,150 mt. On the same day, SHFE warrant inventory decreased by 5,876 mt to 28,166 mt.

Price: On the macro side, US economic data has significantly weakened, with the "US ADP employment data" showing a sharp decline and employment growth of only 62,000. The US economy contracted for the first time since 2022, with Q1 GDP declining by 0.3%. The US March core PCE price index month-on-month rate was 0%, the lowest since April 2020 and below the expected 0.1%. The US economy is currently in a phase where "soft data" has significantly pulled back, while "hard data" remains moderate. Some analysts believe that the weakening of the US economy has some persistence but has not yet fully reached a recession, with copper prices maintaining a slight upward trend. On the fundamental side, from the demand perspective, on the last trading day before the Labour Day holiday, most traders left the market early, reducing market activity. However, just-in-time procurement continued to support premiums. As of April 30, SMM's national mainstream copper inventory decreased by 25,500 mt WoW to 129,600 mt, marking the ninth consecutive week of destocking at an accelerated pace. It has fallen by 247,400 mt from the year's high and by 275,100 mt YoY. Looking ahead to this week, with expectations of cargo replenishment and a decline in downstream consumption sentiment, spot premiums may come under pressure, while inventories may experience a slight buildup. Copper prices are expected to open slightly lower today.

》Click to view SMM Metal Database

[The above information is based on market collection and comprehensive assessment by the SMM research team. The information provided is for reference only. This article does not constitute direct investment research or decision-making advice. Clients should make cautious decisions and not rely solely on this information, as any decisions made are independent of SMM.]